Now that much of Europe has announced its intentions to join the China-led Asian Infrastructure Investment Bank (AIIB), was Washington’s initial opposition a mistake? Assuming the AIIB does get off the ground, what might it mean for future competition between the world’s two largest economies in the arena of global development finance and, by extension, in the realm of soft power? — The Editors

Takaki Yajima-Pool/Getty Images

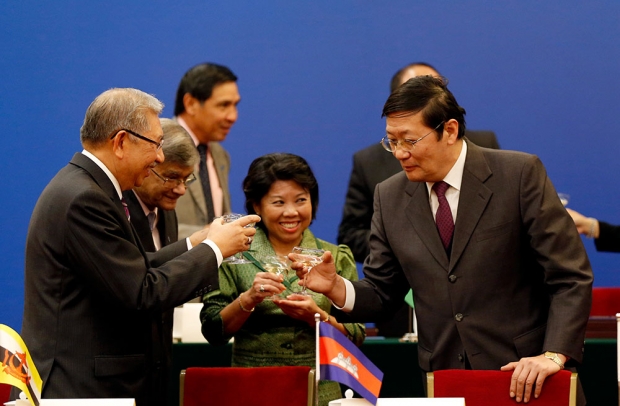

Chinese Finance Minister Lou Jiwei, right, toasts with guests at the signing ceremony of the Asian Infrastructure Investment Bank in Beijing October 24, 2014. More than 20 countries initially signed the agreement establishing the $57 billion bank. A number of other Asian nations including South Korea, Indonesia, and Australia declined to sign on in response to lobbying efforts by the U.S. government.

Comments

Patrick Chovanec

Many of the concerns the U.S. has with China’s Asian-Infrastructure Investment Bank (AIIB) are valid. The problem with developing much-needed infrastructure in Asia is not money—the world is floating in money right now—but selecting and managing projects in way that will deliver the desired results. Given the track record of development lending by China’s existing policy banks (the China Ex-Im Bank and China Development Bank), at best the AIIB risks being merely a vehicle to “buy business” for Chinese companies and absorb China's huge overcapacity. At worst, it threatens to undermine the “good governance” that is key to the region’s genuine economic development. Many of the U.S. allies who broke ranks to join the bank appear—like the U.K., eager to win China's “blessing” as an offshore RMB trading hub—to have done so for deeply misguided and even delusional reasons.

All that said, it’s hard to think of a more ham-fisted and ineffectual way to deal with these concerns than the U.S. employed. It was a classic case of “you can’t beat something with nothing.” The Chinese have accumulated a large pool of savings, and to pretend that Chinese capital won't play a role in the global economy—with or without U.S. permission—is simply untenable. Issuing a blanket “no” to Chinese capital, rather than offering constructive ideas or alternatives, was never going to fly. Strong-arming allies isn't going to work if it looks like China has a plan, and the U.S. is just a carping bystander.

The AIIB potentially has flaws. One of two things will happen: either those flaws will become evident, or China will find a way (perhaps working with other member countries) to overcome them. Either way, China has taken the lead and whining about it isn’t a convincing argument.

If the U.S. wants to lead, then lead. Making progress—and a real commitment—to the Trans-Pacific Partnership (TPP) and the Transatlantic Trade and Investment Partnership (TTIP) is one way to do this. But the Obama Administration, despite pursuing these objectives, has yet to make them a real priority. President Clinton sent Vice President Gore out to debate NAFTA with Ross Perot on live TV. He spent real (and precious) political capital to bat down opposition (much of it within his own party) and ensure congressional passage. By letting pending Free Trade Agreements with South Korea and Colombia twist in the wind for most of his first term, President Obama sent the signal, to friends and foes alike, that his trade agenda wasn't very important, and certainly not worth fighting for.

Into that leadership void has stepped China, with a different vision for the global economy. Can we really blame our friends for taking them more seriously, if we fail to contest that vision in a more credible way?

Zha Daojiong

That the United States is not going to join the Asian Infrastructure Investment Bank (AIIB) is in and of itself not a surprise. But the level of fury in recent weeks Washington has put on public display, is in several ways beyond expectation.

First, China has offered to have a process of negotiation in establishing the AIIB. Among other things, Natalie Lichtenstein, a lawyer who worked at the World Bank for over 30 years, was invited to help prepare the bank’s charter. That gesture alone is indication that China, too, wants the bank to build on experiences and lessons of existing multilateral development banks. After all, being the largest underwriter, China has the greatest stake in seeing the proposed bank start off with a well-thought through institutional structure.

Second, the AIIB is but one among a number of initiatives China has tabled in relating to the rest of the world economy in the same time frame. For example, the pilot Shanghai Free Trade Zone, its follow-up enlargement, and recent expansion to Fujian, Guangdong, and Tianjin, is an indication that China is serious about further liberalizing its own investment and trade policies. In other words, China is demonstrating that it is committed to reform its own policies, rather than just asking others follow it.

Third, it was only a couple of months ago when the United States and China agreed on ten-year multiple visa arrangements for their respective passport holders. This is transformational. Many Western countries followed suit, though to varying degrees. After all, with more convenient international travel, an ever growing number of practitioners of the cross-border trade and investment stand to benefit. When it comes to internationalizing Chinese foreign investment projects, it is investment practitioners, not code drafters, who matter more. Washington’s public disapproval of the AIIB sends out a message of confusion of its intent.

The concerns of the United States and some of its allies about the AIIB not being an exact copy of the World Bank or the Asian Development Bank in governance structure are in some ways understandable. Still, it is hardly convincing to somehow indicate that Washington is in reality saying that a new development institution cannot be innovative.

The last thing China and other founding members of the AIIB want is validation of their critics’ and skeptics’ fears—not just in the outside world but domestically inside China as well. The real test is not so much who is in the AIIB and who is not. Rather, it is whether or not the bank’s proceedings can prevail after its former establishment.

To see the ongoing developments associated with AIIB as a manifestation of competition in soft power between Beijing and Washington is overbearing. After all, no country has money to burn.

For China, it will be ill-advised to see Washington’s disapproval of its allies in joining the AIIB as an affront. As a traditional Chinese saying goes: “One only can be enlightened by listening to both sides, and will end up benighted if one only heeds himself” (jiāntīng zémíng, piān xìn zé àn / 兼听则明,偏信则暗).

For the United States, if it is concerned about the AIIB’s effect on its soft power, it can serve itself better by keeping an open mind about the project. Collaboration on specific investment projects to come will be a plus, too.

Scott Kennedy

In 2005, then United States Deputy Secretary of State Robert Zoellick famously called on China to be a “responsible stakeholder.” He meant that China needed not only to comply with its international commitments, but also to provide public goods to the international community. Well, be careful what you wish for.

Since then China has become much more active in global governance. Chinese occupy leadership positions in a wide range of institutions. In 2013, China helped broker an interim deal in the World Trade Organization’s Doha Round, and in November 2014, China, along with the U.S., made a new pledge to limit carbon emissions, creating momentum heading into the United Nations meeting in Paris later this year. But the Asian Infrastructure Investment Bank (AIIB) is China’s first signature contribution.

China certainly could have done a better job of selling the need for a new development bank. It is still unclear why it would be impossible to improve the quality and quantity of development assistance in Asia through either the Asian Development Bank (ADB) or the World Bank. The arguments that those banks were un-fixable and not open to a greater Chinese role or that China deserves pride of place in a new institution given how much it is contributing leave the impression that the AIIB is a vanity piece or a disguised cash register for Chinese state-owned enterprises.

That said, the U.S. has performed even worse. Although joining the AIIB was not an option since Congress would not have allocated the funds, the U.S. could have adopted the posture of a friendly outside voice. Instead, it discouraged others from joining in the hope the initiative would collapse or leave China with a small “coalition of the willing.” They argued that the bank would not follow international best practices, but in reality it appears the U.S. opposed the AIIB simply because it was a Chinese initiative, full stop. Such knee-jerk antagonism gives life to arguments that the U.S. opposes China’s rise and is bent on containing it. Even more important, American bungling fuels the perception that China can drive a wedge between the U.S. and its allies and that U.S. leadership in Asia is on the wane just when it is needed more than ever.

It’s a shame that China did not provide greater reassurances early on that the bank would not be a tool of Chinese industrial policy and geo-strategic maneuvering, and that the U.S. did not do more to pursue such reassurances and find a way to serve as a constructive supporter. The “best practices” of existing multilateral aid institutions too often have not translated into sustained poverty alleviation and development. There are many other areas of global governance in need of reform, and we can be sure that the AIIB will not be China’s last major initiative. Let’s hope China and the U.S. learn from this experience and find ways to identify areas in need of change where they can collaborate or at least not get in each other’s way, instead of being in opposite camps and forcing others in the region and elsewhere to pick sides. Then both countries will be able to justly claim they are truly acting as responsible stakeholders.

Stephen S. Roach

The Obama Administration has obviously made a major strategic blunder in resisting the establishment of the China-initiated Asian Infrastructure Investment Bank (AIIB). Many of America’s most loyal allies have rejected the folly of this intransigence. By opting to join the start-up of this new international lending institution, they will be much better positioned to shape the governance of the AIIB as insiders rather than voice criticism as outsiders, as the U.S. apparently prefers. Washington’s Cold-War style criticism of its allies for their “constant accommodation” of China is a new and embarrassing low in the China debate.

It is both ironic and hypocritical that Washington’s response is to circle the wagons around the existing Bretton Woods institutions—the IMF and the World Bank. The U.S. Congress has repeatedly dragged its feet on IMF reforms. And lending programs of the U.S.-dominated World Bank have done little to address infrastructure deficiencies in any part of the world. The Asian Development Bank estimates an Asian infrastructure void of some $8 trillion over the 2010 to 2020 period. Clearly new lending capacity is needed to meet this daunting challenge.

Nor does the AIIB pose a threat to more established and experienced international lending institutions. Its initial capital base of $50 billion is less than a third of that which supports the Asian Development Bank and less than a quarter of that held by the World Bank. Surely, an $80 trillion global economy can afford to support much greater lending capacity than is the case today.

But there is a more sinister aspect of Washington’s resistance to this China-sponsored initiative. It is but the latest in an increasingly worrisome string of anti-China actions. The Obama Administration has focused on the Trans Pacific Partnership as its signature initiative on trade liberalization; unfortunately, TPP excludes China, the source of America’s largest trade imbalance. Yet another anti-China currency manipulation bill has been introduced in the U.S. Senate. And there are ongoing frictions over cyber issues, as well as over territorial claims in the China Sea. Suddenly, America’s Asian pivot seems like nothing more than a thinly veiled China containment strategy.

Is the rise of China a risk or an opportunity? Washington is clearly fixated on the threat—all but ignoring the benefits that are likely to come with the emergence of a consumer-led Chinese economy. This shouldn’t be so surprising. History tells us that dominant powers always have trouble with rising powers. Washington is bristling over China’s ascendancy. China, with the baggage of 150 years of a perceived sense of deep humiliation by the West, doesn't take kindly to that reaction. The AIIB folly only deepens concerns over an increasingly troubled relationship. A rethink by Washington is urgently needed.

Mikko Huotari

From a European standpoint, the current debate about China’s AIIB initiative seems overblown. If we move beyond the media hype, we are not witnessing the beginning of the end of the U.S.-led global financial order. Neither do we see a major political re-orientation of U.S. allies across the globe, certainly not in Germany.

Nevertheless, the ongoing institutionalization of AIIB and the surrounding political maneuvering provides the U.S. and European countries with a learning opportunity. It’s a fact to be recognized: the global financial order is undergoing fundamental changes and the further regionalization of development financing is just one dimension of this transition. New initiatives to provide financial asistance in times of crisis as well as the broader structural transformation of the international monetary system will repeatedly confront us with a similar set of challenges. The expectation that nothing will change would indeed be foolish. Fortunately, most experts, including the other contributors to this conversation, seem to agree on that.

Obviously much more U.S.-European and intra-E.U. communication and coordination is needed to manage the necessary changes and also the public diplomacy side of this transformation. It is indeed remarkable how little real dialogue and concrete transatlantic initiatives have materialized since 2007/2008 beyond the relatively stagnant G20 coordination and the difficult joint management of the Euro Crisis.

Some observers frame adaptation in global financial order simply as an issue subordinate to existing military alliance patterns. This is not a particularly fruitful starting point for the much needed dialogue. And of course, specific material interests of European countries differ: With regard to the policy agenda of the AIIB, Europe has much more immediate interests than the U.S. in the infrastructural development of the Eurasian continent not least because the EU is a leading exporter of construction services.

More profoundly, both Europe and the U.S. heavily depend on the success of China’s structural transformation, of which the AIIB and other financial initiatives by China are an external manifestation. In fact, the AIIB is just one of the mechanisms of China’s ongoing and welcome experimental financial internationalization in which a flurry of outbound financing instruments are currently being tested. Attempting to block precisely the one initiative that comes closest to “Western” understandings of international financial governance does not seem a wise strategy. On the contrary, the AIIB in its multilateral shape should be seen as a “victory of the system,” the result of Chinese learning and as another channel to further integrate and socialize China into multilateral rule-making.

We need to work with China not against it. Framing issues in black or white, with or against “us” will not help in the long run. The competition that AIIB and other China-centered initiatives will pose is a wake-up call to strengthen and adapt the existing institutions to new realities. It also challenges us to find better ways to improve the linkages and networking of complementing financial arrangements and forms of currency cooperation. Efforts at keeping China at bay in international rule-making for the 21st century will almost certainly backfire and reinforce Chinese determination to circumvent the existing order.

Wu Jianmin

People around the world are talking about the failure of U.S. strategy with regard to the Asia Infrastructure Investment Bank (AIIB) initiated by China. What went wrong? As I see it, three things did.

First, a misreading of the features of today’s world: a misreading the name of the game of our time and a misreading of the trends in world development. For most of the last century, a zero-sum game theory dominated the practice of international relations. The world witnessed two World Wars, and many regional wars and revolutions. The Cold War followed World War II and featured a confrontation between the two superpowers of the day, the United States and the Soviet Union. If the U.S. won, it would mean a Soviet loss. If the U.S.S.R. won, then the U.S.A. would be seen to lose. Over time, people of the world became sick and tired of the tension. Towards the end of the last century, this game theory gradually lost its appeal and was replaced by the positive-sum game. We went from confrontation to win-win cooperation.

There are dual factors behind this change. First, globalization makes nations deeply interdependent. The interests of different countries are profoundly intertwined. If one tries to hurt the other side, it will suffer the pain, too. It’s no longer an I-win-you-lose scenario. Second, common challenges face mankind—climate change, terrorism, natural disasters, drug trafficking, and pandemics, to name but a few. No country, no matter how powerful, is able to cope with these challenges alone. The human race is bound to unite for its survival.

What is the trend in world development? Today we are no longer living in a uni-polar world. It is moving towards multi-polarity. The U.S. is no longer in the position to dictate how others should behave. Issues concerning the future of mankind are to be discussed and resolved democratically by all countries involved. Is the U.S. aware of this trend? Does Washington try to adapt to it? I hope America will stop misreading the trends of world development and adapt to the trend towards multipolarity.

After misreading, next came misjudgement. Some Americans suspect that China’s initiative to set up the AIIB is aimed at the U.S. They asserted that the new bank would undercut the World Bank, the International Monetary Fund, and the Asia Development Bank, and increase China’s leverage in the Asia-Pacific region. I would remind those people that China is a member of the World Bank, the IMF, and the ADB. How could China want to hurt these international financial institutions? China’s intention in proposing to launch the AIIB is to generate growth in Asia, the global growth center. Infrastructure is the key to the growth and Asia’s demand in this respect is huge: about $8 trillion from 2015 to 2020. Obviously, the existing international financial institutions are not able to meet this demand. If the infrastructure demand in Asia, especially East Asia, is met, it is bound to stimulate growth. Growth in the Asia-Pacific region will in turn help generate growth in the U.S., Europe, all of Asia, Africa, and Latin America. If the AIIB proves a success, it surely will become a classic example of a positive-sum game and win-win cooperation.

Further misjudgment concerns the degree to which traditional U.S. allies will continue to “obey” their “big brother.” During the Cold War, most U.S. allies stood firmly by Washington’s side. With the Cold War over, that kind of obedience is gone.

Finally, misbehavior. First, the U.S. refusal to join the AIIB. The second misbehavior was to try to prevent U.S. allies from joining the would-be new bank.

Misbehavior is a ogical consequence of misreading and misjudging.

What should Washington do now? I hope that common sense will prevail in Washington. People can make mistakes. No one is infallible. When one realizes one’s mistake, the smartest thing to do is to correct it as soon as possible. China keeps saying that the door is open for the U.S. to join in the AIIB. I hope the U.S. will do it. This is not a matter of losing face. If the U.S. stays put, it will lose more face. It’s up to Washington to make the choice.