Cement is the most widely used substance on the planet after water. It is also one of the most polluting—producing between 5-8 percent of global greenhouse gas emissions, more than twice that attributed to aviation. Cement’s carbon footprint increases every year with huge demands for building materials, particularly in China, India, and large parts of the developing world.

In some ways, the global cement industry has been more receptive to the green agenda than some fossil fuel energy companies and large utilities. Cement makers have signed up to voluntary emissions cuts, reassured they will play a key role producing the materials needed for a low carbon world—from building hydropower dams to fixing wind turbines.

At the Paris climate summit last year, Heidelberg Cement and 16 other cement manufacturers went further and promised to decarbonize their production by 2030. The effort, they claimed, will lead to a 10 percent worldwide reduction in carbon dioxide (CO2) emissions.

But demand for cement is growing faster than emissions per tonne are falling, leading to an overall increase in emissions. What’s more, two thirds of the sector’s emissions come from the chemical reaction induced when cement ingredients are mixed in the kiln. This means the industry’s environmental headache will only grow.

“We are convinced we have to do something on CO2 emissions in a proactive way,” said Rob van der Meer, public affairs director on global environmental sustainability for Germany’s giant Heidelberg Cement, one of the world's largest producers.

So far, Heidelberg has made cuts by boosting the energy efficiency of its operations, replacing coal with renewable alternatives such as biomass and waste material, and substituting a proportion of emissions-intensive clinker in cement with cleaner materials.

But all these processes have their limitations. “All of this will result in 30 percent reductions in emissions by 2030 from 2005 levels—but this is not enough to limit to (a rise in global warming to) 2C,” says van der Meer.

A more radical solution is needed. Some scientists have proposed ways to produce “carbon zero” cement using binding agents derived from oil and silicon. California-based Calera Corp has even found ways for cement production to absorb more carbon than it releases, similar to how certain corals produce reefs by excreting dissolved calcium carbonate or limestone.

But none of these new technologies have achieved commercial success or been proven at scale.

The Case for CCS

The industry has latched on to Carbon Capture and Storage (CCS) technology as its insurance against future curbs on carbon. CCS is an umbrella term for a range of methods to suck carbon dioxide from the atmosphere at the point of source and store it underground. But some critics see the idea as a non-starter because it locks dirty fossil fuel power plants into future energy systems and deflects funding for renewable alternatives. However, advocates point out there is a big difference in using CCS for industrial processes, for which there are no alternatives so far.

“There will be carbon capture... We see it as a necessity for our sector, we cannot escape it,” said van der Meer.

It’s not just the cement industry. Scientists and climate researchers are warning that the world can’t meet the Paris targets and cap global warming at 2C without developing new technologies to suck carbon dioxide out of the air. The IEA views the technology as the most cost-effective way of delivering around a fifth of required global carbon reductions (based on a certain number of CCS plants being operational by 2050).

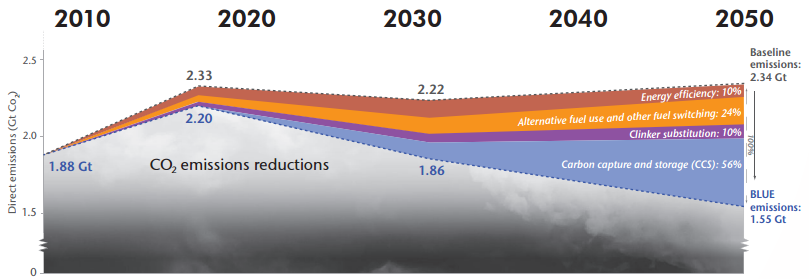

Cement Sector CO2 Emissions Reductions Below the Baseline, Low Demand, Scenario, 2010-2050

All of these technologies need to be applied together if the BLUE scenario targets are to be achieved—no one option alone can yield the necessary emissions reductions.

Industrial CCS is the cornerstone of the European Commission’s plans to cut emissions 95 percent by 2030. It is also a key part of the U.K.’s energy strategy to meet its own climate targets enshrined in law, given the country’s dependence on oil and gas.

However, the necessary funding and support has failed to emerge.“It’s a desperate situation” says Jonas Helseth, policy officer at Bellona, a Norwegian think tank: “Lack of action on CCS is undermining the world’s ability to counter climate change.”

Pilots

Heidelberg has thrown itself into CCS research and development, in collaboration with the European Cement Research Academy. In Norway, they have finished testing a carbon capture project at the major NORCEM cement factory last year in Brevik, and are now waiting for the government to figure out a funding mechanism to develop a full-scale demonstration project.

The project will capture 50 percent of emissions by extracting CO2 out of the cement plant’s smokestack flue gas. If all goes to plan, the plant will become Norway’s third operational CCS project by 2020, catching up to 400,000 tonnes of CO2, piping it for storage in an underwater continental shelf, or converted into low carbon biofuel for transport.

The Norwegian government has provided 75 percent of the €12 million (90 million yuan) investment, and Heidelberg hopes this will act as a blueprint for future production plants with carbon capture.

Another cement pilot plant is being developed by a consortium of companies at Lixhe in Belgium, funded by the European Commission, as well as pilots in Texas and Taiwan.

Fits and Starts

But despite the emergence of some projects, delays, rising costs, and protests have plagued the development of CCS since the Norwegian energy giant Statoil proposed the concept more than two decades ago.

Pilot projects have floundered across Europe. To the shock of investors, last year the U.K. government unexpectedly pulled £1 billion (9.6 billion yuan) of funding from the White Rose CCS Commercialisation project, weeks before the final bid.

Without further government funding, the Norwegian project is out of the question, Heidelberg’s van der Meer admits.

Storage Woes

The dilemma of where to put the captured carbon is similar to that of where to bury nuclear waste. The Brevik project has been plagued by protests by locals worried about the disastrous consequences of stored CO2 escaping even from a deep geological deposit.

The plant, incidentally, was the scene of one of Norway’s worst pollution accidents in 2001 when at least 750 tonnes of toxic sludge poured into the local harbor and fjord waters. Local authorities have refused the use of the harbor and mine to store carbon because it is close to a large population of people.

“CCS is basically about taking a problem and stuffing it away under the carpet,” Rasmus Hansson, parliamentary leader of Norway’s Green party has said in a recent interview with The Guardian. “We will then live with the statistical risk of some gigantic underground burp.”

The immense costs of building CCS projects, and rock bottom prices for carbon in the E.U.’s dysfunctional Emissions Trading Scheme (ensuring the incentives for CCS are weak), further threaten the future commercial viability of the technology.

Leakage

Cement makers have more immediate concerns of their own. If competitors in Eastern Europe, Turkey, and Asia flood the market with cheap cement, CCS becomes a less attractive option.

“It will increase our costs by 50 percent and our competitors outside of Norway will come into the market with cheap cement,” says van der Meer.

The China Question

If cement is going to clean up its act, a lot rides on what happens in China where 60 percent of global cement is produced—at the moment mostly from old-fashioned small plants with coal-fired, smoke-spewing furnaces.

CCS is a key part of China’s national climate change program—but apart from investing in a cement pilot in Texas, the focus has been on curbing emissions from coal-fired power plants rather than cleaning up heavy industry.